Test a strategy on data it has not seen.

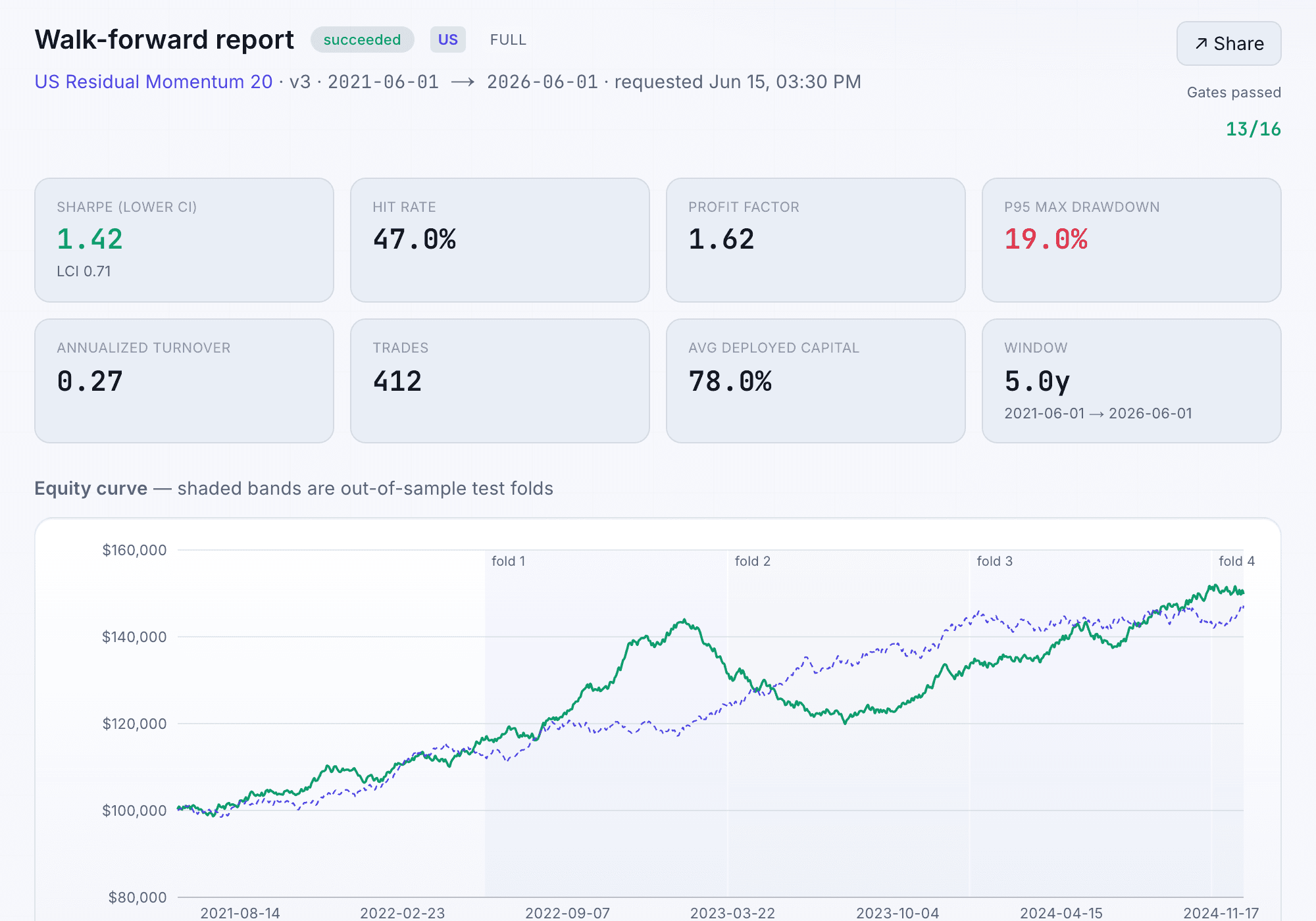

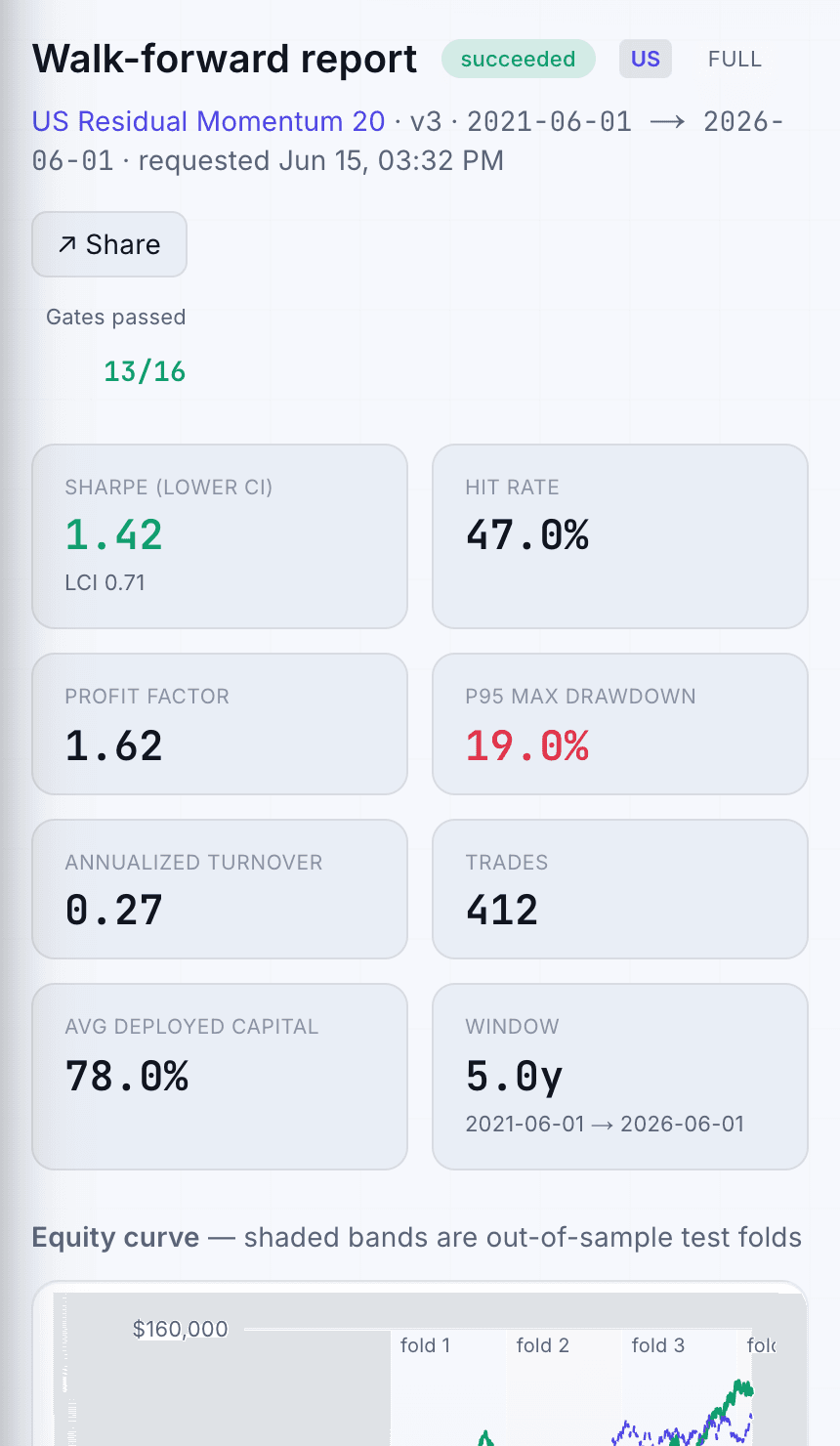

Run walk-forward, out-of-sample tests with trading costs and overfitting checks. Each result shows the universe, assumptions and qualified performance measures.

Walk-forward backtesting, live at app.tradepolaris.com/backtests

Walk-forward, not curve-fit

Rolling out-of-sample folds, next-bar-open fills, gap-aware stops, bid/ask spread, square-root market impact and short-borrow costs.

An institutional tearsheet

Equity curve vs the S&P 500, Sharpe / Sortino / Calmar, drawdown, VaR / CVaR, a monthly heatmap and a 6-factor attribution.

Is the edge real?

Probabilistic & Deflated Sharpe, minimum track-record length, and Probability of Backtest Overfitting separate a real edge from luck.

Build it your way.

Use the visual builder, write Python or export the signals. Every route uses the same validation engine.

From point-and-click to production Python.

Every strategy runs through the same walk-forward tests and overfitting checks.

- No-code builder. Set factors, exits, optimisers and risk models.

- Python SDK. Use a sandboxed runtime with full control.

- Export your work. Take the spec, rule sheet or Pine output with you.

strategy: momentum-x-sectoruniverse: { region: US, top: 500 }signals: - momentum(126) - momentum(21) - filter: adx(14) > 20portfolio: { long: 50, weighting: risk_parity }exits: { trailing: 8%, invalidation: signal_flip }validate: { walk_forward: 5y, costs: realistic, gates: [DSR, PBO] }

Ask the market your first question.

Sign up for beta access and create your account in seconds.

Join beta →Backtested / walk-forward results are hypothetical, do not represent actual trading, and are not indicative of future results.