Aladdin-grade risk, for your own book.

Aegis turns any portfolio — a basket, your paper book, or a saved strategy — into an institutional risk cockpit: ex-ante VaR/CVaR and factor-risk decomposition, scenario & stress testing, an efficient-frontier optimizer, regime detection and multi-strategy sleeve portfolios. It recomputes live as you edit, and writes you a plain-English read of what's driving the risk.

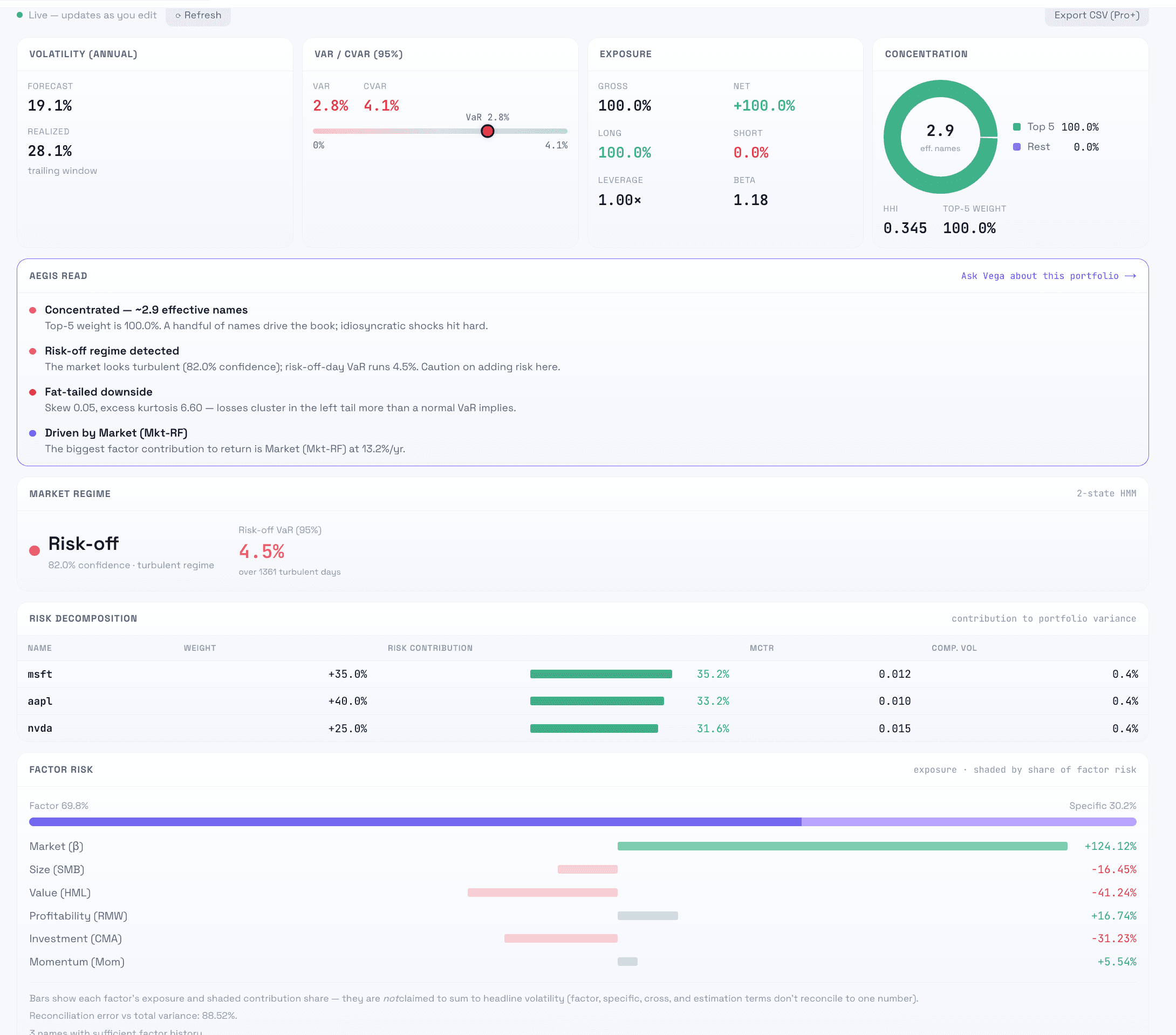

Portfolio Risk Cockpit

Ex-ante VaR/CVaR with seeded Monte-Carlo, per-name risk contribution (MCTR / component-VaR), factor-risk decomposition, correlation and concentration, liquidity, rolling risk over time and fat-tail analytics — live as you edit.

Scenario & stress testing

Replay real crises (COVID-2020, 2022 rates, SVB), apply macro/factor shocks across rates, credit, oil, USD and vol, or run a fat-tailed Monte-Carlo — see the P&L and the worst contributors instantly.

Institutional optimizer

An efficient frontier plus one-click suggested allocations — minimum-variance, maximum-Sharpe, risk-parity, HRP, minimum-CVaR — each scored against your current book, with Black-Litterman views and sector/turnover constraints.

Regime, attribution & sleeves

A risk-on/off market-regime read with regime-conditional VaR, portfolio-level factor return attribution, and multi-strategy sleeve portfolios that net and risk-budget across strategies.

Explore more

Ask the market your first question.

Sign up for beta access — create your account and start in seconds.

Join beta →Backtested / walk-forward results are hypothetical, do not represent actual trading, and are not indicative of future results. Trading is paper (simulated) only. Not investment advice.